What company or industry do you want us to cover?

We want to create a community of investors, make sure to subscribe and share!

Investment Thesis

Consumers are now expecting action immediately without any hassles or time delays. Every industry in the world is subject to disruption, and real estate is next on the chopping block.

Company Description

OpenDoor is a digital platform for residential real estate. This platform enables customers to buy and sell houses online. It generates revenue through home sales, along with other revenue from real estate services.

Qualitative

Overview

Sector: Real Estate

Industry: Digital Platform Sales

Competitors: Zillow, Redfin, Transactly

Strategy: Create an Efficient Home Selling Marketplace

OpenDoor’s primary business intention is to buy a house in cash from a seller and flip it to a buyer.

They do not have a buyer immediately lined up but attempt to flip the house as quickly as possible.

Closing with the seller takes only 15-20 days.

OpenDoor allows the home seller to sell on their timeline, whether they need 30 days or 6 months until they close the sale and move out.

Business Model: Delight their Customer

OpenDoor’s Net Promoter Score (% of customers to recommend service) is 70%.

This 70% score is on the same level as Netflix and Apple, signaling their customers love the product.

90% of sellers use OpenDoor without an agent, customers trust the brand.

Market: Residential Real Estate

The US residential real estate market has yearly sales of $1.3 Trillion.

88% of home buyers purchase homes through an agent, significantly more than the 69% of purchases in 2001.

Using the numbers above, real estate agents grossed between $55 Billion and $70 Billion (5%-6% fees assumed).

This is important because this is the cut that Open Door is trying to take.

Moat: First Mover Advantage

The company was founded in 2014 and was the first digital marketplace for residential real estate.

In their S1 filing, they outlined they have sold 4.4x more homes than their next competitor.

In 2019 they sold nearly 19,000 homes.

Since its inception, it has sold $10 billion and served over 80K homes.

This first-mover advantage is imperative because of its brand implications.

Their total gross home sales speak volumes about their appeal to homeowners.

X-Factor: Data

OpenDoor completely reaches the price based on their propriety algorithm.

This algorithm considers the location, appliances, structural integrity, and features of the individual home.

The more data the better. When they earn a more significant amount of data, OpenDoor can eventually completely control their margins with scale.

They can control their margins because they will have enough data to know exactly how much the house should sell for on both ends and how long it could sit on the market.

They are trying to turn residential home buying and selling into a complete science – not an art form.

Cash Cow: Fee Structure

OpenDoor’s fee structure is comparable to traditional real estate agents, though on occasion they could become as high as 10%.

While there is no significant difference between the fee structures of agents and OpenDoor, the immense value that OpenDoor offers is worth the extra potential fees to their customers.

Even with these high fees, their conversion rate is still 35%.

The average conversion rate for traditional real estate agents is close to 1%.

This is not necessarily an apples-to-apples comparison, but it shows that when someone wants to sell a house and OpenDoor is in the conversation, they have a higher likelihood of converting.

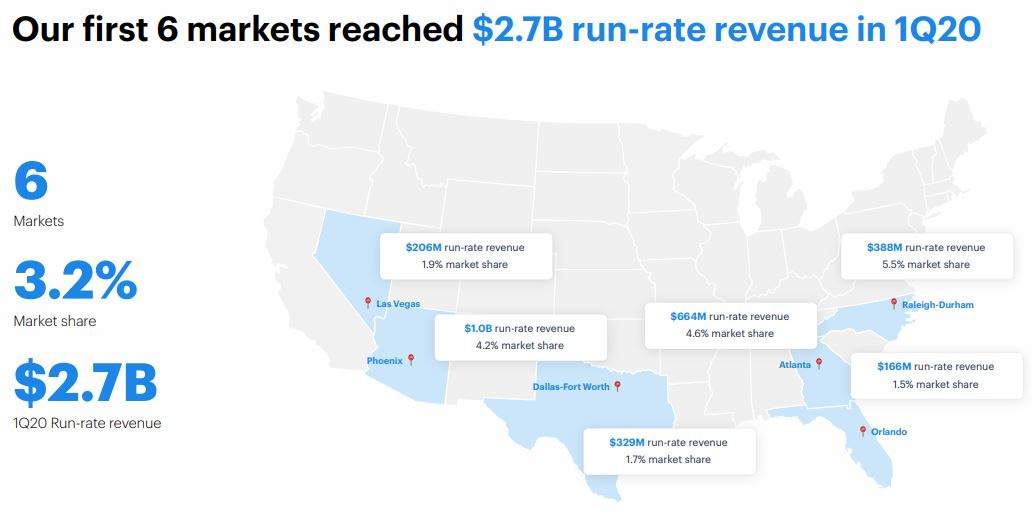

Growth Opportunities: Geographical Market

This new-founded unicorn is only in 21 US markets.

They have nearly no presence in the midwest, or the northern portion of the east coast (New York, Boston area).

In their first 6 markets (pictured below), they own a reported 3.2% market share.

If they can begin to successfully penetrate other US markets, that 3.2% market share in the largest markets could spark hypergrowth in the company over the next few years.

Quantitative

Since this company is a SPAC (Special Purpose Acquisition Company), we do not have access to their direct financial statements.

We can not provide key financial health or profitability ratios.

Risks

Wholesale real estate flipping is a highly capital-intensive business.

High-risk factor if OpenDoor is not able to sell the house quickly after purchase, interest from the bank could drastically hurt the bottom line.

Reliant on the cyclicality of the real estate economy.

The balancing act of pleasing the seller (Could hurt bottom line), OpenDoor making a larger profit (Seller could be upset about the money lost, hurting customer loyalty rating), and compromising on both ends (forcing a quick sell to both buyer and seller).

Learn Something

Residential Real Estate Conversion Rate

“Fallacy of the OpenDoor Business Model”